Insurance Quotes

Free Auto Insurance Comparison

Compare Quotes From Top Companies and Save

Even though you’re required to have car insurance in all states, the Insurance Research Council confirms that roughly 14% of the driving population is uninsured. States with the highest levels of uninsured motorists include:

- Mississippi: 28%

- New Mexico: 26%

- Tennessee: 24%

- Oklahoma: 24%

- Florida: 24%

While driving without insurance is simply unacceptable and could get you in trouble with the law, many drivers make an equally detrimental mistake in driving underinsured. If you have the minimum amount of insurance coverage for your vehicle, it may not be enough to protect you and your valuable assets in the case of an accident.

At times like these, it pays to explore all insurance options – including full coverage car insurance.

While full coverage car insurance isn’t a one-size-fits-all solution, it will provide coverage for any physical damage incurred to your car during an accident. Even if you are at fault in a crash, full coverage insurance will pay for vehicle repair. If repair costs more than the value of your car, it could also pay for a complete vehicle replacement. There are many cheap full coverage insurance options.

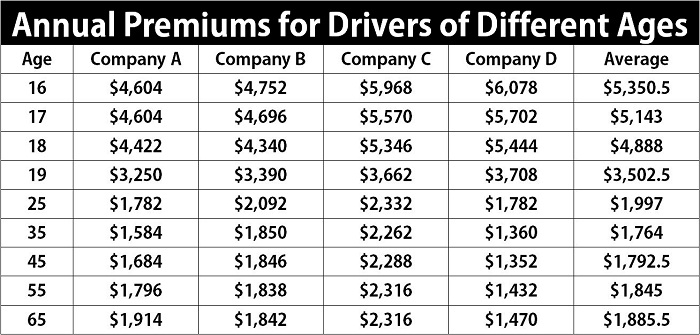

Full coverage car insurance isn’t a requirement in any state, but it could save you money out-of-pocket in a more serious accident. The amount of money you pay for full coverage insurance will vary greatly, often lowering with age, as seen in the chart below:

A young 16-year-old driver could pay as much as $6078 a year for car insurance compared to a 35-year-old driver with an annual premium as low as $1360. There are several factors that will influence how much you pay for full coverage insurance, which we will discuss on this page. There are many ways for you to get cheap full coverage auto insurance that is significantly lower than the prices above.

What Full Coverage Car Insurance IS

Now it’s time to dig a little deeper. You’re probably quite familiar by now with the term “liability insurance.” If a vehicle only carries liability insurance, this indicates the minimum amount of insurance coverage that is required in the majority of states. At its core, liability insurance will pay for any damage a driver causes to property or other people in an accident.

In comparison, full coverage indicates a greater amount of car insurance coverage on a policy above and beyond liability and will include:

- Collision: Just like it sounds, collision will provide coverage in an accident, no matter whose fault it was. An insurance company will pay for damage to your vehicle based on the actual cash value of your car, tallied at the cost of vehicle replacement minus depreciation and minus your insurance deductible.

If the other insurance company is found liable in an accident, they will use the same formula to pay for damages to your car. Once again, collision coverage isn’t required by law, but it may be required by a financial institution if you’re still paying on a car loan or lease.

- Comprehensive: Comprehensive coverage covers all the extras in vehicle damage from hail, fire, flood, storm, or theft. If your car is totaled because of a natural disaster, the same formula will be used as indicated above to determine how much will be paid out in vehicle damages.

Comprehensive insurance coverage may also pay for minor cosmetic issues like a cracked windshield or broken window glass. Comprehensive coverage is not required by law but can offer added protection in a full coverage policy.

And speaking of legal requirements… Each state will have a different minimum requirement by law for car insurance regarding both property damage and bodily injury liability. This insurance is required for drivers that cause an accident and must pay for the injured party’s property damage and medical expenses up to a certain limit.

As an example, you may live in a state like Florida with minimal liability insurance requirements at $10,000 for medical costs for each injured individual with a $20,000 accident limit. Insurance will also pay for up to $10,000 in property damages, listed as 10/20/10.

Enter your ZIP code below to view companies that have cheap auto insurance rates.Free Auto Insurance Comparison

You can find the most common minimum insurance requirements by state listed below:

- 10/20/10: Florida, Louisiana, Oklahoma

- 12.5/25/7.5: Ohio

- 15/30/5: California, Delaware, New Jersey, Pennsylvania

- 15/30/10: Arizona, Georgia, Nevada

- 20/40/5: Massachusetts

- 20/40/10: Alabama, Connecticut, Hawaii, Michigan, West Virginia

- 20/40/15: Illinois, Iowa, Maryland, Texas

- 20/50/10: Idaho

- 25/50/10: Indiana, Kansas, Kentucky, Missouri, Montana, New Mexico, New York, Oregon, Tennessee, Vermont, Washington, Wisconsin

- 25/50/15: Arkansas, Colorado

- 25/50/20: Virginia, Wyoming

- 25/50/25: Mississippi, Nebraska, New Hampshire, North Dakota, Rhode Island, South Dakota, South Carolina

- 25/65/15: Utah

- 30/60/10: Minnesota

- 30/60/25: North Carolina

- 50/100/25: Alaska, Maine

Average car insurance rates by state are estimated at (source AARP.com):

Even if full coverage insurance isn’t required by a lender on a new car, you may decide to choose full coverage over liability insurance to avoid the headache of paying for vehicle damage out-of-pocket.

When determining whether or not you can afford full coverage car insurance, keep in mind that rates may fluctuate greatly based on:

- Amount of coverage. Full coverage isn’t necessarily a blanket term that can be used to describe a specific type of auto insurance; in comparison to liability insurance, full coverage will provide additional levels of coverage that may meet full state or financial lender requirements. The more coverage you add to your policy, the more insurance prices will increase.

- State of residence. As listed above, minimum car insurance requirements will vary greatly by state. Even if you happen to change ZIP Codes within your state of residence, your full coverage insurance could become higher or lower based on local statistics that include construction, accident percentages, traffic, and crime rate.

- Payment frequency. If you plan to pay monthly for your full coverage insurance, your insurance rates will be significantly more expensive than paying quarterly or biannually. Paying more upfront in insurance costs will help you to save more money over a policy term.

- Amount of deductible. If you have the money in your bank account to increase your deductible – the amount you are responsible for paying before insurance coverage kicks in – full coverage car insurance rates could drop even further. If you currently have a low deductible of $250, raising the deductible to $1000 could keep insurance costs reasonable, if you can afford it.

Other factors that impact car insurance rates may include:

What Full Coverage Car Insurance IS NOT

Full coverage insurance policies will vary from provider to provider, which is why it literally pays to shop around. If a full coverage insurance policy seems inexpensive at face value, it may not include bodily injury coverage; this is a common omission in the insurance industry.

Depending upon your insurance provider and state requirements, full coverage insurance may not cover:

- Uninsured/Underinsured Motorists: If you don’t take the time to delve into your full coverage insurance policy, it’s easy to overlook added protection in uninsured or underinsured motorist coverage. Uninsured motorist insurance coverage is beneficial if you are in an accident that is caused by an uninsured driver.

Without insurance, an uninsured motorist may not be able to pay for medical and vehicular damage expenses. Uninsured motorist coverage in a full coverage policy will compensate for your injuries, lost wages, and pain and suffering in an accident. An uninsured driver policy will often cover underinsured drivers with lower liability limits to provide fair coverage.

- Car Rental/Towing: Towing is often packaged in with a full coverage insurance policy for convenience. However, it’s important to check that this coverage is included so that you aren’t left stranded and in need of roadside assistance.

Some insurance companies may offer limited car rental reimbursement in a full coverage policy, while others do not. If you believe that you will need a car rental in the future – if your vehicle is in an accident, for example – additional coverage can be added onto a policy.

- Gap Insurance: After buying a new car and signing up full coverage insurance, it is naïve to assume that gap insurance is automatically included in a policy. Nonetheless, gap insurance is critical to protect against loss when vehicle depreciation is compared to the amount owed.

Full coverage car insurance is intended to pay the actual cash value of a car; gap insurance will bridge the gap to pay the amount left between what you owe and what the car is actually worth.

- Vanishing Deductible: Today, a number of insurance companies offer an attractive vanishing deductible that will “disappear” as a reward for a good driving record. However, the insurance tacked onto an advertised vanishing deductible may not offer full coverage on a vehicle.

Make sure to discuss the specifics of a vanishing deductible reward with your insurance agent before an accident occurs; in some cases, an extra charge will be added onto a policy to provide full coverage eligibility.

Once again, it’s important to emphasize that a full coverage insurance policy will vary significantly from company to company. Reading the fine print of your policy in detail before signing on the dotted line will guarantee that you are protected from bumper to bumper the next time you’re on the road.

Depending upon your individual policy, some full coverage exclusions may apply.

For example, if you raise the deductible on your full coverage policy, it could negate full glass coverage altogether. In most cases, damage to glass in a vehicle is automatically covered under the comprehensive portion of full coverage insurance. The deductible amount you choose on a policy could affect the amount of glass coverage.

As a final word of warning, watch for the phrase intrafamily exclusion in your full coverage policy. This clause could indicate that you will only be protected with limited coverage in an at-fault accident with a motorist that is uninsured or underinsured. As a result, your family’s medical expenses will not be covered.

Coverage that was typically found under an uninsured or underinsured motorist policy in full coverage auto insurance now has lapses in protection based on intrafamily exclusion. Available expenses covered may be capped at a modest dollar amount, costing you thousands of dollars extra in uncompensated medical bills.

What Are the Benefits of Full Coverage Insurance?

Taking the time to research the benefits you can receive from a full coverage insurance policy can do a world of good. Understanding your insurance policy inside and out can eliminate serious stress and financial heartache in the case of an accident.

Here are several important benefits that you can expect to receive from signing up for a full coverage car insurance policy:

- Protection for you and any other driver of your vehicle under your insurance policy.

- Insurance coverage for all personal belongings in a vehicle, like electronics, luggage, and valuables.

- Waived collision deductible when an accident involves two or more vehicles within the same insurance company.

- Insurance benefits paid upfront without a mandatory waiting period.

- Stereo equipment covered in an accident up to a set amount if installation meets insurance guidelines.

- Lost wage reimbursement during court proceedings related to an accident.

Even taking into account the many benefits of full coverage insurance, there may be times when it is to your advantage to stick with liability auto insurance. Full coverage insurance may not make sense for a car that is not driven regularly and is stored in a garage. An older vehicle that doesn’t have any value also won’t warrant the expense of a full coverage insurance policy.

If full coverage insurance isn’t a requirement from a lender, you can base your final decision between full coverage car insurance and liability insurance on:

- Cost of vehicle and replacement

- Full coverage compared to liability insurance rates

- Amount of money in savings

- Amount of deductible

It often comes down to a numbers game.

If your car has a value of $15,000 with $700 paid per year in full coverage insurance and a $750 deductible, full coverage can be worth your while. As a vehicle decreases in value, the expense of full coverage insurance may no longer merit the additional payment.

To make a final decision, consider your peace of mind when you get behind the wheel. There are plenty of ways to get low cost full coverage auto insurance. If your car meets the criteria for full coverage insurance, it only makes sense to protect yourself and your vehicle with more than enough insurance coverage every time you’re on the road.

Here are a few great safety guides:

Texting and Driving: A National Epidemic

The Truth about Teen Driving

Safe Driving Tips for Seniors

Car Seat Safety Tips

Safe Driving With Dogs